6 最小二乘线性回归法

6.1 相关概念

- 因变量(Dependent variable,Y):依赖于其它变量的变化而变化,响应变量;

- 自变量(Independent variable,X):可以直接控制的变量,协变量;

- 有监督学习的数据表示:\(D=\{(x_1,y_1),\cdots,x_n,y_n)\},x\in R^p,y \in R\);

- 模型(model):函数;

- 参数(Parameters):参数是添加到模型中用于估计输出的成分;

6.2 线性模型

因变量的值由独立自变量之间的线性数学模型决定。\[y=\beta_0+\beta_1\times x_1+,\cdots,+\beta_p\times x_p\],模型表示:

\[\begin{bmatrix} y_{1} \\ y_{2} \\ \cdots\\ y_{n} \end{bmatrix}\] = \[\begin{bmatrix} \beta_0 \\ \beta_0 \\ \cdots \\ \beta_0 \end{bmatrix}\] + \[\begin{bmatrix} x_{11} & x_{12} & \dots & x_{1p} \\ x_{21} & x_{22} & \dots & x_{2p} \\ \cdots & \cdots & \cdots & \cdots\\ x_{n1} & x_{n2} & \dots & x_{np} \end{bmatrix} \times \begin{bmatrix} \beta_1 \\ \beta_2 \\ \cdots \\ \beta_p \end{bmatrix}\]模型的矩阵表示: \[Y=X\beta\]

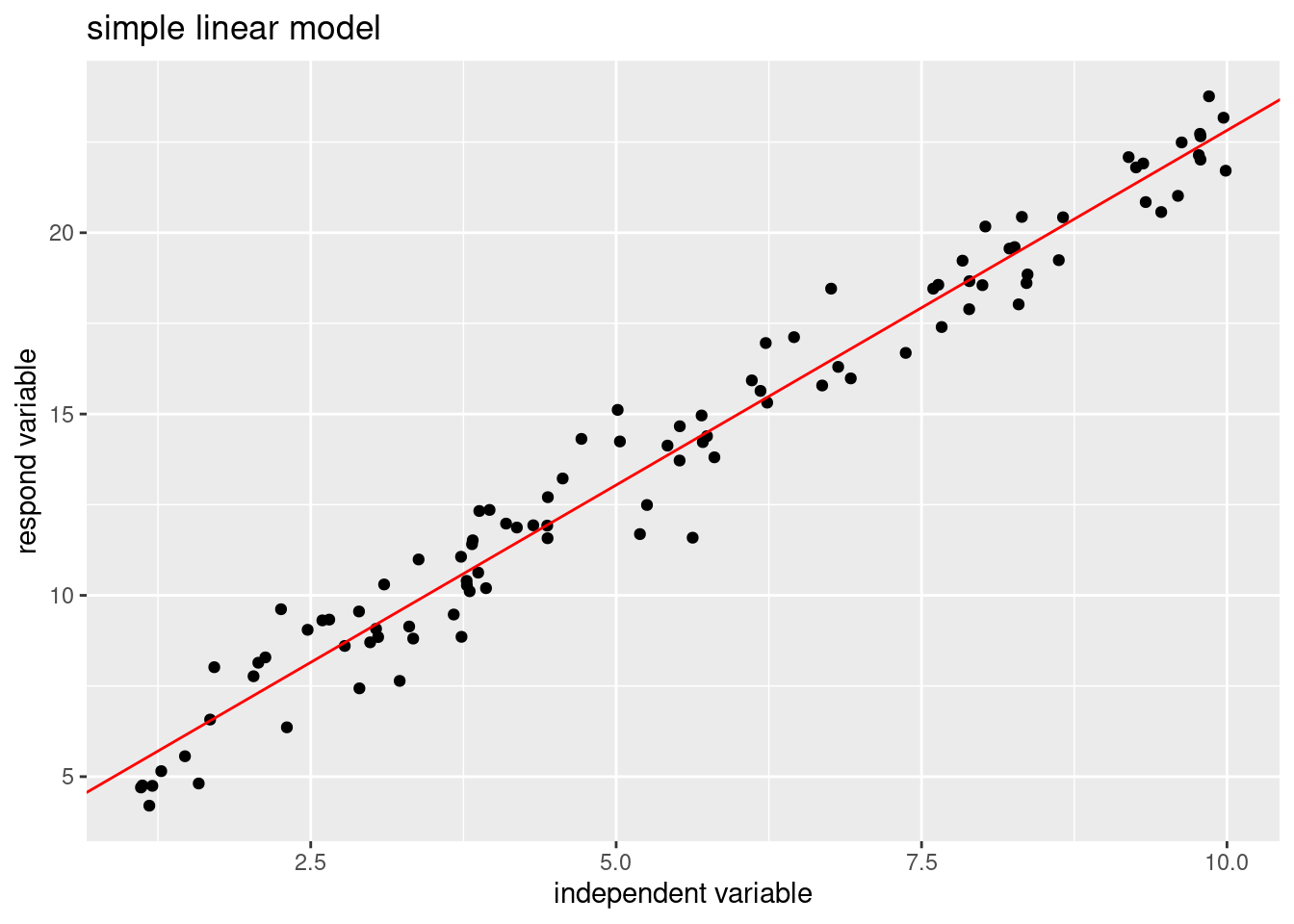

6.2.2 简单线性模型(Simple Linear Model,SLM)

- y响应变量为连续型变量;

- x是自变量,只包含一个变量;

- \(y_i=\beta_0 + \beta_1*x_i+\epsilon_i\)

library(ggplot2)

# Simulated data produced

x <- runif(100,1,10)

y <- 3+2*x+rnorm(100,0,1)

data_slm <- data.frame(x=x,y=y)

head(data_slm)## x y

## 1 3.820282 11.410064

## 2 2.031977 7.768217

## 3 6.686440 15.786684

## 4 3.825949 11.517779

## 5 8.219747 19.563085

## 6 3.305819 9.139702##

## Call:

## lm(formula = y ~ ., data = data_slm)

##

## Residuals:

## Min 1Q Median 3Q Max

## -2.67746 -0.73960 -0.02542 0.70193 2.04759

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 3.26171 0.21803 14.96 <2e-16 ***

## x 1.95611 0.03615 54.12 <2e-16 ***

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 0.9605 on 98 degrees of freedom

## Multiple R-squared: 0.9676, Adjusted R-squared: 0.9673

## F-statistic: 2928 on 1 and 98 DF, p-value: < 2.2e-16

# visual the model

ggplot(data_slm,aes(x,y))+geom_point()+

geom_abline(slope=fit_slm$coefficients[2],

intercept=fit_slm$coefficients[1],

color="red")+

labs(x="independent variable",y="respond variable",title="simple linear model")

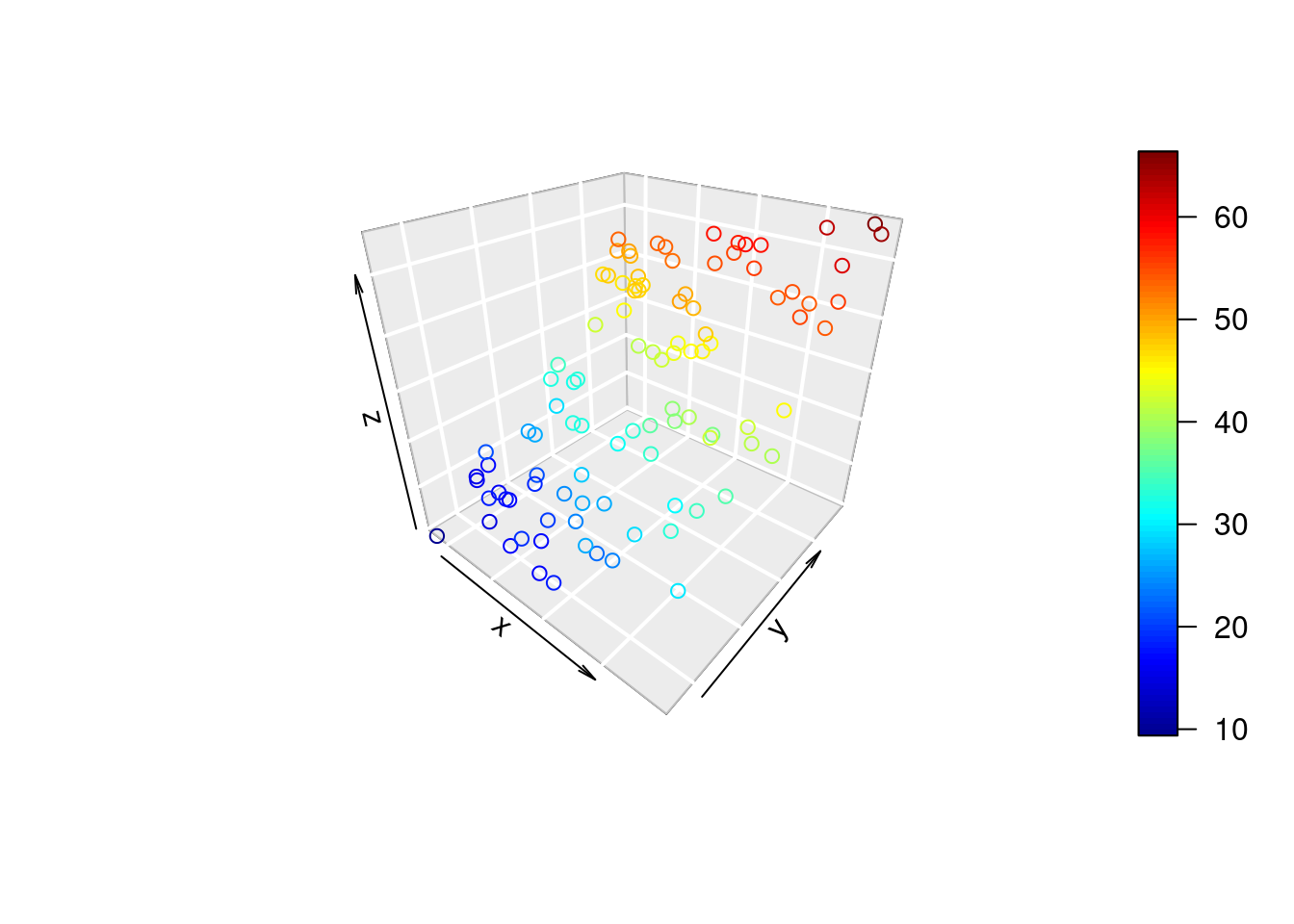

6.2.3 多元线性回归(Multiple Linear Model,mlm)

- y响应变量为连续型变量;

- x是自变量,包含多个变量(至少是2个及以上);

- \(y_i=\beta_0 + \beta_{11}*x_{i1}+\cdots+\beta_{ip}*x_{ip}+\epsilon_i\)

# Simulated data produced

x1 <- runif(100,1,10)

x2 <- runif(100,1,10)

y <- 2*x1+5*x2+rnorm(100,0,2)

data_mlm <- data.frame(x1=x1,x2=x2,y=y)

head(data_mlm)## x1 x2 y

## 1 9.853459 4.560755 40.79412

## 2 7.513059 1.981255 23.88531

## 3 2.939099 2.653477 16.51904

## 4 4.763115 1.569623 19.18558

## 5 9.060682 4.849449 42.43664

## 6 6.809352 5.105696 38.95931##

## Call:

## lm(formula = y ~ x1 + x2, data = data_mlm)

##

## Residuals:

## Min 1Q Median 3Q Max

## -4.2790 -1.3993 -0.1574 1.1783 5.5516

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 0.27466 0.63596 0.432 0.667

## x1 2.00130 0.07774 25.744 <2e-16 ***

## x2 4.95841 0.07444 66.605 <2e-16 ***

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 2.017 on 97 degrees of freedom

## Multiple R-squared: 0.9806, Adjusted R-squared: 0.9802

## F-statistic: 2454 on 2 and 97 DF, p-value: < 2.2e-16

# install.packages("plot3D")

library(plot3D)## Warning in fun(libname, pkgname): couldn't connect to display ":0"

scatter3D(x=data_mlm$x1,y=data_mlm$x2,z=data_mlm$y,phi = 30, bty = "g")

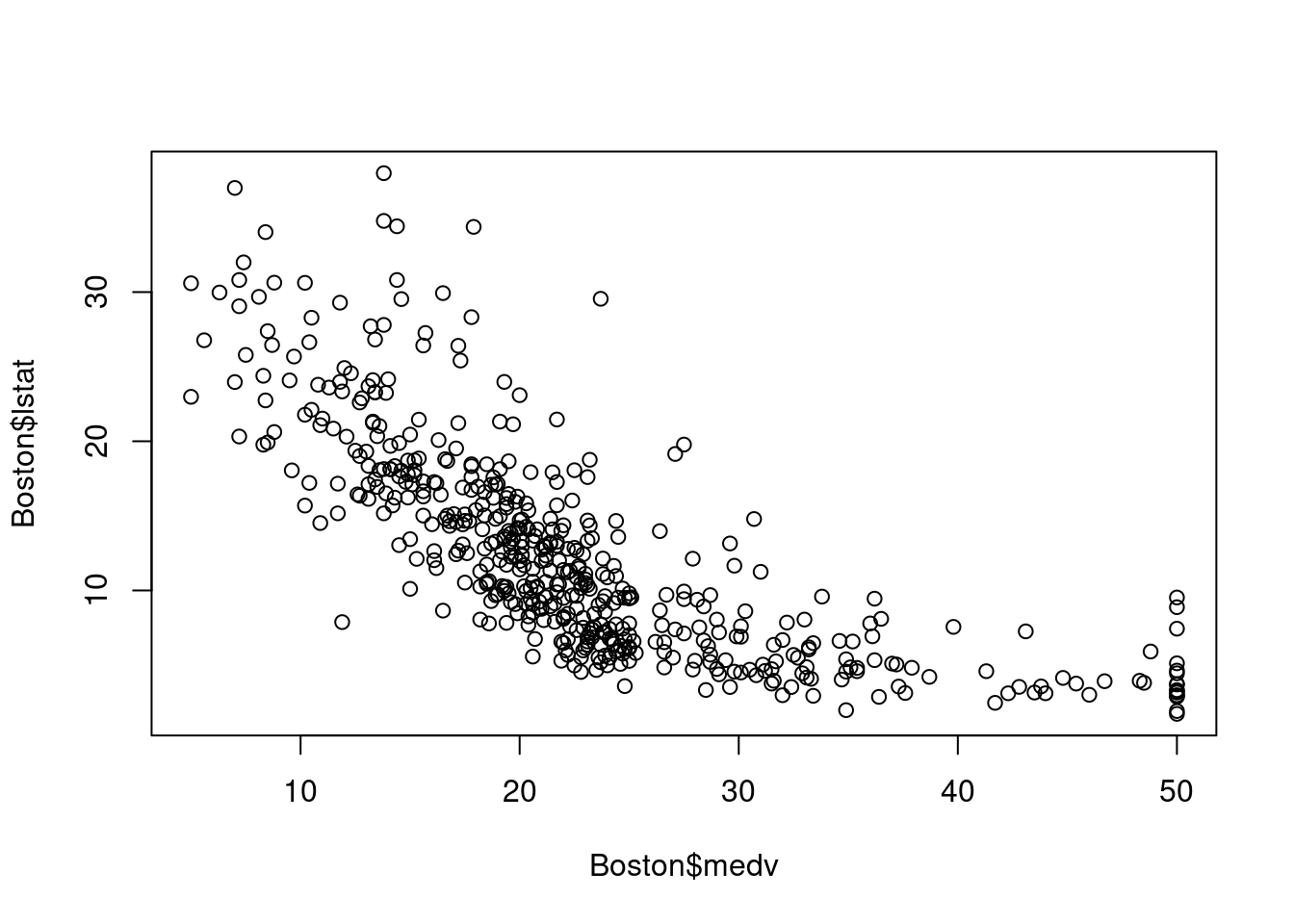

6.2.4 回归实例

- 使用MASS库中所带的波士顿房价数据,其中的因变量为房价的中位数,自变量为房龄、房间数等,想预测房价。

## [1] "crim" "zn" "indus" "chas" "nox" "rm" "age"

## [8] "dis" "rad" "tax" "ptratio" "black" "lstat" "medv"

plot(Boston$medv,Boston$lstat)

##

## Call:

## lm(formula = Boston$medv ~ Boston$lstat, data = Boston)

##

## Residuals:

## Min 1Q Median 3Q Max

## -15.168 -3.990 -1.318 2.034 24.500

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 34.55384 0.56263 61.41 <2e-16 ***

## Boston$lstat -0.95005 0.03873 -24.53 <2e-16 ***

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 6.216 on 504 degrees of freedom

## Multiple R-squared: 0.5441, Adjusted R-squared: 0.5432

## F-statistic: 601.6 on 1 and 504 DF, p-value: < 2.2e-16

# multiple variance regression

mlm.fit <- lm(Boston$medv~Boston$lstat+Boston$age,data=Boston)

summary(mlm.fit)##

## Call:

## lm(formula = Boston$medv ~ Boston$lstat + Boston$age, data = Boston)

##

## Residuals:

## Min 1Q Median 3Q Max

## -15.981 -3.978 -1.283 1.968 23.158

##

## Coefficients:

## Estimate Std. Error t value Pr(>|t|)

## (Intercept) 33.22276 0.73085 45.458 < 2e-16 ***

## Boston$lstat -1.03207 0.04819 -21.416 < 2e-16 ***

## Boston$age 0.03454 0.01223 2.826 0.00491 **

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Residual standard error: 6.173 on 503 degrees of freedom

## Multiple R-squared: 0.5513, Adjusted R-squared: 0.5495

## F-statistic: 309 on 2 and 503 DF, p-value: < 2.2e-16- 结果解释:变量之间独立的情况下,系数就为影响程度,若存在多重共线性,则系数的解释比较复杂。